Research

Nov 12, 2025

Exploring the Merger and Acquisition Landscape Within Web3

Introduction

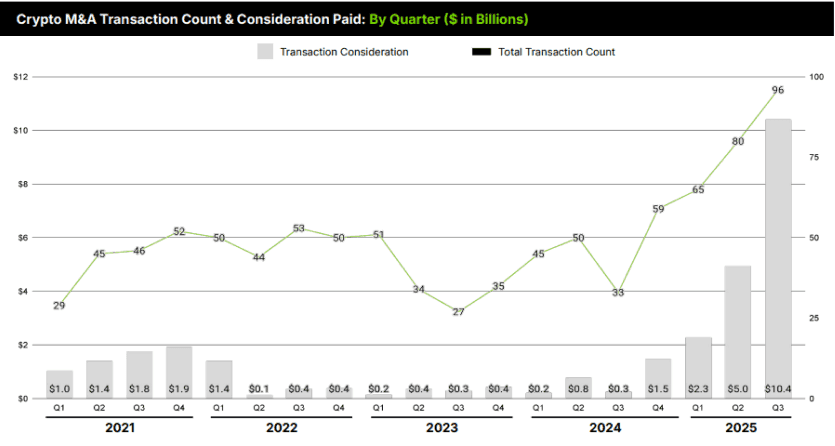

M&As in crypto are increasingly being used as an entry ticket into the industry, with deal activity now higher than ever. After a considerable deal quantity decrease in 2022 to 2023, value has increased considerably into 2025 as both crypto-native and traditional players have been using acquisitions to grab licenses, infrastructure, and distribution channels. Quarterly deal counts are up from 27 (Q3 2023) to 59 (Q4 2024) and hit 96 by Q3 2025, with disclosed value climbing to over $10.4B across the first three quarters of 2025.

Structurally, Web3 deals still look a lot like traditional ones, functioning mainly with cash or equity-based deals, with tokens seldom added into the mix. The main difference lies in governance and integration: some transactions can involve DAO approval, and post-merger work can include aligning tokenomics or migrating on-chain assets. This report maps who’s buying what and why in Web3, how deals are being paid for, and what that means for institutions looking for ways to gain exposure and for founders deciding whether to build, partner, or sell.

M&As In Web2

Mergers and acquisitions (M&As) are the process of combining companies or even assets to accelerate growth, expand capabilities, or foster synergies that make the merged entity worth more than the individual parts. A merger and acquisition typically goes through robust strategy, due diligence, valuation, and financing processes, as well as post-merger integration activities.

There are several common structures used in M&A transactions, each of which defines how ownership and value transfer will take place:

Acquisition: when an acquirer absorbs the bought company fully, including all its assets and operations. Day to day operations are maintained under the acquirer company’s brand and image, thus requiring it to adapt the acquirer's products and operations into the acquirer’s systems.

Merger: the two companies consolidate to form a completely new, single unit. Day to day operations may involve a combination of systems, services, cultures, and management in which both companies share power and resources.

Asset Purchase: it’s a transaction in which the buyer company acquires specific assets and liabilities of the target company, rather than the company itself. In practice, the acquirer gains ownership of the whole company, including tangible and intangible assets, intellectual property, and contracts. This type of acquisition can be more complex, but allows the acquirer to avoid the purchase of unwanted liabilities or underperforming parts of the acquiree’s business.

Stock Swap: a transaction where the acquirer company exchanges its shares for the shares of the acquired company. The shareholders of the target receive shares in the acquiring company, often based on a predetermined swap or exchange ratio that reflects the relative valuation of the two companies.

M&As in Web3

In Web3, M&As can look like traditional corporate acquisitions of companies in which for example a DEX acquires a stablecoin payments processor, but they can even take the form of protocol-level mergers such as when the blockchains Klaytn and Finschia combined to create a single blockchain: Kaia, creating a unified ecosystem. The goal is often to consolidate liquidity, user bases, or technology stacks to strengthen capabilities across the acquirer’s ecosystem.

While equity and cash remain the dominant consideration in Web3 M&As, token based deals, including token swaps or equity-plus-token mixes are also possible and have happened before like when Avail acquired Arcana and the deal was structured as a token swap at a 4:1 ratio.

Token Swaps: akin to stock swaps in traditional M&As, this is a deal structure often seen in crypto mergers and acquisitions, when a protocol acquires or merges with another, and instead of traditional equity or asset purchase, projects exchange respective tokens between their communities. Token swaps in crypto M&As can have varying ratios that define how many tokens of one project are exchanged for tokens of another, and it’s a critical part of the negotiation as factors like market caps, token supply, project valuations, revenue, and even user base are still taken into consideration for the deal.

Key differences between Web2 and Web3 M&As

Deal structures can be more flexible and often consist of a mix of equity, token swaps, and on-chain asset transfers. The payments themselves might involve stablecoins, project tokens, or a hybrid structure where investors and contributors from both sides are compensated in the merged project’s new token. The negotiation phase can also differ and in many cases, on-chain governance must also be employed where approval may be required by token holders instead of a corporate board or shareholder votes. This makes M&As in Web3 not only financial transactions but also community-based events, requiring alignment between technical teams, investors, and decentralized stakeholders.

Once approved, the integration process goes beyond merging operational systems and bookkeeping, characteristic of traditional M&As. It often involves merging codebases, combining or migrating treasuries, and aligning tokenomics to prevent dilution, technical overlaps, or conflicting incentives. Protocols may undergo smart contract redeployments, cross-chain bridge updates, or liquidity migrations to ensure continuity across user bases and DeFi integrations. From this point of view, M&A execution in Web3 becomes a combination of engineering, legal coordination, and community management, where success depends as much on technical precision and communication as on deal-making itself.

Web3 Mergers & Acquisitions Market Size

Total Volume Of M&As in Web3

Web3 M&A Growth Rate

After a rough decline of 49% in deal count per quarter from the peak in Q3 of 2022 with 53 deals to only 27 deals in Q3 of 2023, the crypto M&A activity increased again as both Web3 and traditional players position themselves for the next phase of industry growth. This increase is not only in deal count, but also in the types of deals being made and what type of businesses acquirers are targeting.

Web3 acquirers are primarily engaging in vertical integrations. They are often purchasing trading venues, brokerage and payment platforms, and essential infrastructure providers. A notable example is OKX’s license purchase through a MiFID II-licensed Malta firm, which exemplifies how exchanges are using regulated entities to broaden their product offering and geographic presence.

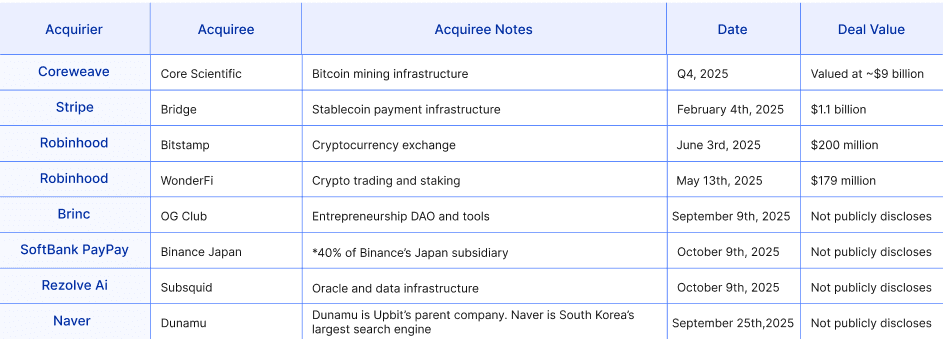

On another hand, Web2 buyers are entering the market by acquiring consumer-facing gateways that already have large user bases and they can easily expand. These deals reflect how these companies are leveraging their capital to buy their way into the crypto industry rather than building products from scratch. The perfect example for this is how Naver, essentially the South Korean Google, acquired Dunamu in September 25th, the parent company of Upbit, in a stock-swap transaction whose value was not publicly disclosed. This showcases how large, established companies prefer to leverage their capital to buy their way into the industry through already proven and regulated businesses, rather than building products from scratch for their already-massive user bases.

It is evident that from a strategy standpoint, Web2 and Web3 acquirers are approaching M&As with fundamentally different objectives. Web3 firms are focused on improving their efficiency and gaining control with existing products, strengthening their infrastructure and licensing to scale vertically. While in contrast, Web2 firms are seeing M&A of crypto firms as a shortcut to market entry, leveraging their financial strength to acquire distribution and credibility in a sector they can’t build into as quickly.

Based on Architect Partners’ Crypto M&A Tracker, activity has sharply increased from a low experienced in Q3 of 2023. Deal volume has climbed from 27 deals in Q3 2023 to 59 in Q4 2024, and has continued to rise all the way to 96 deals in the first three quarters of 2025. Disclosed deal value followed the same path, jumping from under $1 billion per quarter to to $2.3, $5, and $10.4 billion across the first three quarters of 2025. Year-over-year deal growth:

Q1’25 vs Q1’24: 65 vs 45 = +44%

Q2’25 vs Q2’24: 80 vs 50 = +60%

Q3’25 vs Q3’24: 96 vs 33 = +191%

This acceleration suggests the crypto industry has moved from defensive pivots to strategic expansion. Buyers are pursuing acquisitions to strengthen their infrastructure, secure regulatory licenses, and gain access to solid user bases. Larger deal sizes also indicate greater interest for scale and integration rather than small asset picks. The rising pace also reflects better funding conditions, stronger balance sheets, renewed VC support, and a more stable macro backdrop.

Overall, the 2025 trend points to a maturing market where M&A is acting as a primary driver of growth and ecosystem entry.

Key Mergers & Acquisition Deals and Players

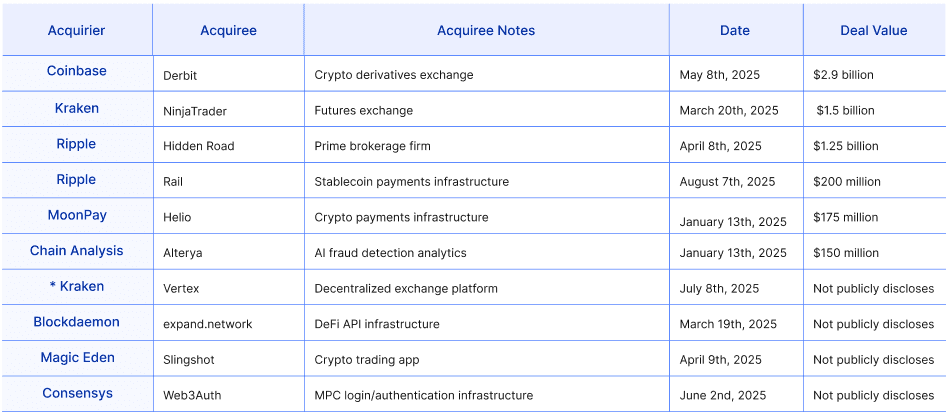

Web3 --> Web3 Acquisitions | Relevant M&A’s YTD

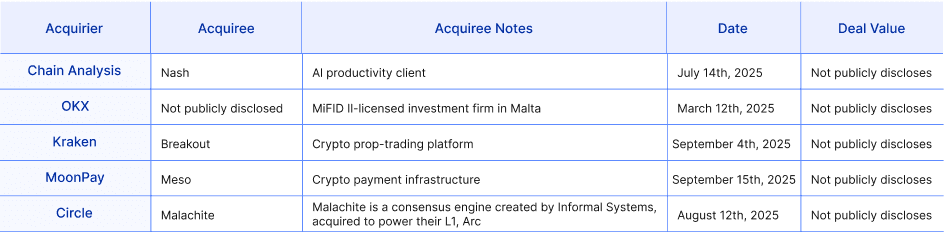

Web2 --> Web3 Acquisitions | Relevant M&A’s YTD

Top Acquirers Within The Last 2 Years

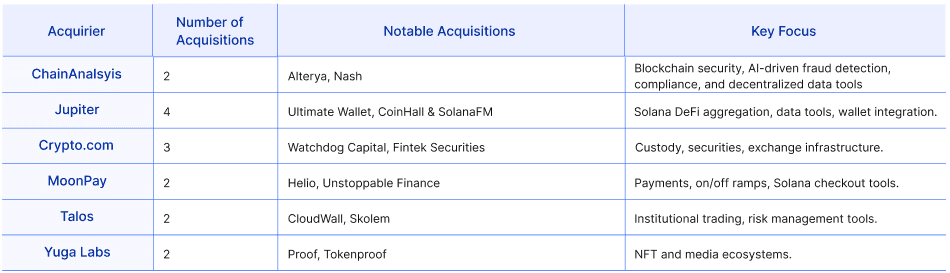

From January 2024 to now, the Web3 M&A landscape includes a couple of acquirers that were more active than others: Phantom, Sol Strategies, and WonderFi, each targeting acquisitions that give them an edge in key layers of crypto infrastructure. Rather than spreading across new narratives, these firms seemed to be doubling down on their own niches. Phantom stands out with four acquisitions, all on Solana, aimed at building a full-stack consumer product: a secure wallet, NFT and data indexing, trading tools, and even fraud prevention. WonderFi made three acquisitions, FX Institutions, Bitbuy, and Blade Labs, to merge key parts of Canada’s crypto ecosystem under one brand with the simple goal of combining regulated exchanges, institutional services, and developer tools to create a single, compliant platform that can serve different audiences. These acquisitions highlight vertical expansion, not spreading onto new categories. Together, they represent how some firms are leveraging M&As to vertically improve their ecosystems, controlling gateways, and tightening their product offering.

In short, the top acquirers over the past two years are not chasing hype or significantly embarking onto new sectors, but consolidating their distribution channels and infrastructure. Wallets are becoming super-apps, validators are becoming financial hubs, and exchanges are becoming regulated infrastructure providers to expand their geographic reach. This indicates that the nature of M&As isn’t speculative, but more strategic, revenue-driven tactics.

Key Trends Within Web3 M&A Deals

By category: Which Narrative is Leading?

Based on the report by Architect Partners, exchanges & trading infrastructure held the most M&As in Q3 of 2025. Deal counts remained overall steady at 15 and 16 per quarter between Q4 2024 to Q3 2025, respectively, but value did change significantly: transaction sizes jumped from $25M in Q4 2024 to $1.42B in Q3 2025.

In short, what’s getting bought more intensively are derivatives venues, brokerage licenses, trading platforms and UIs, and payment/fiat rails. The spike in value in Q3 2025 is caused by large-sized deals though, and the lower numbers in the other quarters are likely because of undisclosed transaction values.

What are the Predominant Deal types in Web3 M&As?

When it comes to deal structures in Web3-related M&As, they don’t differ considerably from traditional deal structures: most transactions are still carried as plain company acquisitions paid in cash, stock, or a mix of both. All-cash is still common for regulated financial entities such as exchanges and brokerages, while larger strategic buys often use a mix of cash and stock.

However, a Web3-specific characteristic is that deals may include project tokens alongside equity. Examples of this type of structure so far this year are Magic Eden and Slingshot (equity + $ME tokens) and Ripple and Hidden Road (cash + XRP + equity), but those are basically the exception based on disclosed data, indicating that it’s not the most common. Infrastructure and engine acquisitions often look like asset and team-hiring deals (e.g. Circle and Malachite). There’s also minority equity stakes instead of full takeovers (PayPay’s acquisition of ~40% in Binance Japan). In the end, equity and cash are the most dominant type of deal, while token components appear only in a few cases where there is ecosystem alignment.

What is valued in Web3 M&As?

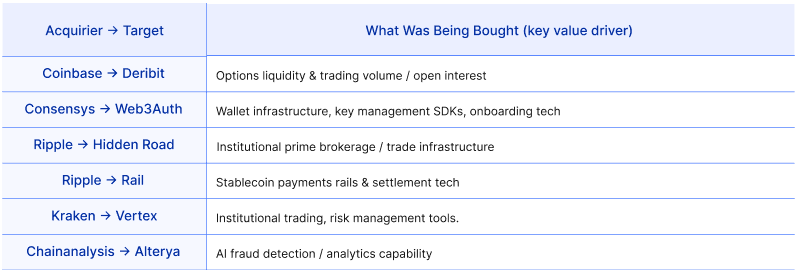

In Web3 M&As, what is often valued for a company to be acquired is real on-chain usage, regulated distribution capabilities, and essential infrastructure. Based on the most relevant acquisitions from this year, acquirers are focusing on regulatory access, market distribution, liquidity and volume, infrastructure IP with a strategic edge, and capable teams, not just token metrics or community hype.

For example, Coinbase’s $2.9 billion purchase of Deribit hinged on Deribit’s dominance in options trading volume and open interest, which are metrics tied closely to revenue potential and institutional traction. Consensys’ acquisition of Web3Auth wasn’t about raw user counts, but about their ability to embed wallet and key-management infrastructure into MetaMask, the on-ramp technology and SDKs were being bought. And Chainalysis, MoonPay, Blockdaemon’s acquisitions were about AI fraud engines, API connectivity, or payments plumbing, which are core tech components that scale.

Conclusion

For institutions, the revival of M&A represents an attractive and more compliant path into the industry, a way to gain regulated exposure, infrastructure, or distribution without having to build from scratch. By acquiring established, licensed, or technically proven teams, investors and institutions can mitigate their operational and regulatory risk while effectively accelerating their entry into on-chain markets.

For founders, the renewed deal flow means M&A has become a real strategic option again. Strong teams and products can position themselves as acquisition targets by focusing on regulatory readiness, sustainable revenue, active user bases, and strong technical advantages. Whether teams decide to build independently, partner, or sell now depends less on hype cycles and more on alignment with potential acquirers that are looking for ways to strengthen their infrastructure, compliance, and ecosystem depth rather than entering the market for mere speculation.